Budget Execution Overview

Budget execution is the process by which the financial resources made available to an agency are directed and controlled toward achieving the purposes and objects for which budgets were approved. The process involves compliance with both legal and administrative requirements. OMB Circular A-11 provides detailed instructions on all aspects of budget execution.

The General Accounting Office publication, Principles of Federal Appropriations Law, is a comprehensive reference regarding the basic principles of appropriation law. It discusses the statutes and regulations governing appropriations matters and references significant decisions rendered by the Comptroller General and the courts. Each operating unit budget office should have a copy of this document available for reference.

Principles of Federal Appropriations Law discusses the use of budgetary resources in terms of availability as to purpose, time and amount. According to this concept, the legality of an expenditure depends on three things:

- the purpose of the expenditure must be proper;

- the obligation must occur within the time limits applicable to the appropriation; and

- the obligation must be within the amounts Congress has established.

Proper budget execution requires compliance with these three principles. The instructions contained in Circular A-11, if properly followed, will assure that budget execution in the agency meets required standards. 31 U.S.C. 1301 and 1341 provide the basic legal framework for budget execution.

Section 1301 provides that "appropriations shall be applied only to the objects for which the appropriations were made." A single appropriation account may provide funds for numerous programs and activities, thus providing an agency considerable discretion in spending the money. Nevertheless, agency spending is usually guided by the justifications presented to the Appropriations Committees; and the enacted appropriations bill and accompanying reports.

Section 1301 also states that an appropriation in a regular, annual appropriation law remains available only for that fiscal year unless the act "expressly provides that it is available after the fiscal year covered by the law in which it appears" or the appropriation is for rivers and harbors, lighthouses, public buildings or the pay of the Navy and Marine Corps.

Section 1341 prohibits obligation or expenditure in excess of the amount appropriated and the incurring of obligations in advance of appropriations, except as "authorized by law".

Steps in Budget Execution

- 1. Financial Plans: The agency's financial plan is the first phase of budget execution. The President's Budget is the framework of the initial financial plan and should be internally updated through the various phases of Congressional action leading to enactment. Per Section 120.21 of OMB Circular A-11, financial plans must accompany all apportionment and reapportionment requests to OMB.

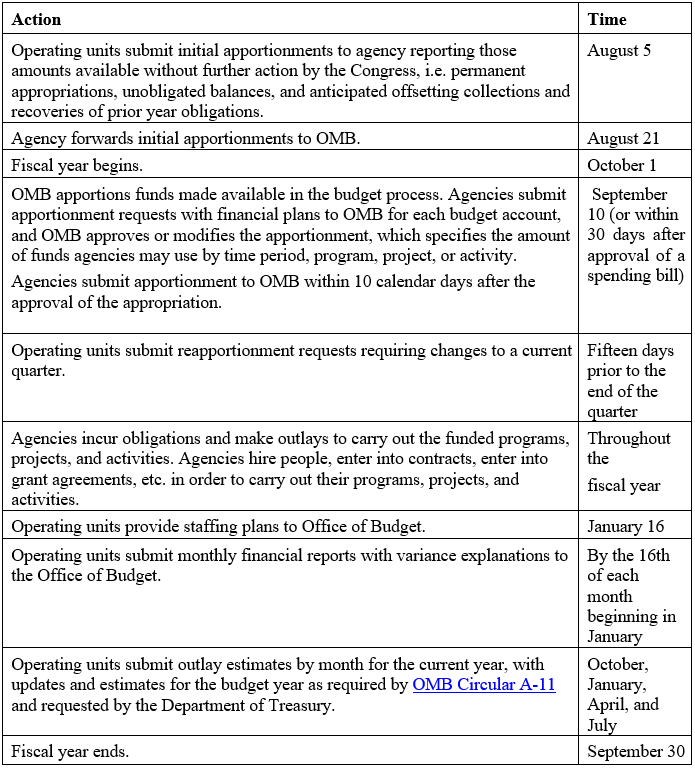

- 2. Apportionments and Reapportionments: Except in a few cases as provided by law, funds contained in appropriations legislation and other funds, (including reimbursements, recoveries of prior year funds, and carryover funds) may not be obligated until they are apportioned. See Section 120 of Circular A-11 for additional information on exceptions. Apportionment requests prepared by agencies are not valid until OMB approves the apportionment. Usually, the signature of the appropriate OMB official constitutes approval. Exceptions are: emergencies involving the safety of human life or the protection of property for which OMB may provide telephone approval of apportionments under Section 120.35 of OMB Circular A-11; and adjustments not requiring submission of a reapportionment request and which are considered to be "automatically apportioned" as provided under Section 120.36 of the Circular. Agencies then allot the apportioned funds among their operating units or other administrative subdivisions. When the level of funds provided changes, (supplemental appropriations, extensions of continuing resolutions, enactment of full year appropriations, etc.), agencies must prepare reapportionment requests and receive OMB approval before the funds may be obligated.

- 3. Reports on Budget Execution: Accounting officers prepare and certify reports on budget execution. Part 4, II of Circular A-11 provide instructions for preparation and use of budget execution reports.

- 4. Other Requirements: Agency also prepare outlay plans and reports and respond to Congressional Directives. If an account includes a deferral or a rescission proposal, operating units prepare a variety of additional material. Reprogrammings require another set of information. These subjects are covered in Circular A-11.

An apportionment is an Office of Management and Budget-approved plan to use budgetary resources (31 U.S.C. §§ 1513–b; Executive Order 11541). It typically limits the obligations the federal government may incur for specified time periods, programs, activities, projects, objects, etc.

Read More: Execution - Step 16 Budget Apportionment

Part IV, II, Section 130 of OMB Circular A-11 provides detailed instructions on preparing the Report on Budget Execution (S.F. 133) for most accounts, including credit programs.

Read More: Execution - Step 17 Reports on Budget Execution

A rescission is enacted legislation which cancels previously enacted budget authority before the authority would otherwise lapse. A deferral is any action or inaction by an officer or employee of the United States Government that temporarily withholds, delays, or effectively precludes the obligation or expenditure of budget authority.

Read More: Execution - Step 18 Rescissions & Deferrals

Agency will report and monitor its financial condition throughout the year. The purpose of outlay monitoring is to reduce the Government's interest costs.

Read More: Execution - Step 19 Monitoring Federal Outlays

Financial plan details out agency's execution plan throughout the year. 31 U.S.C. 1514 requires that each agency have a system of administrative control of funds.

Read More: Execution - Step 20 Financial Plan

Reprogramming process is to realign funds within an appropriation or fund account to use for different purposes than those contemplated at the time of appropriation.

Read More: Execution - Step 21 Reprogramming

A Congressional Directive reflects legislative intent.

Read More: Execution - Step 22 Congressional Directives